Hyperbolic Discounting: Why Smart Women Choose $10 Today Over $22,605 Tomorrow

Imagine I offered you a choice.

You could keep an extra $10 in your pocket this month.

Or you could have $22,605 in the future.

Most of us would immediately choose the second option.

After all, the math seems obvious.

Yet, every single day, intelligent, capable, financially responsible women make the opposite choice -- not because they're careless with money, and not because they don't understand the value of investing.

They do it because they're human.

And humans are wired with a fascinating psychological bias known as hyperbolic discounting.

This bias quietly influences almost every financial decision we make, from investing and saving to spending and debt repayment. It causes us to place a disproportionately high value on immediate rewards while undervaluing rewards that exist in the future.

The result is that a small pleasure today can feel more important than a much larger benefit tomorrow.

Not because it actually is, but because our brains make it feel that way.

What Is Hyperbolic Discounting?

Behavioral economists use the term hyperbolic discounting to describe our tendency to discount future rewards based on how far away they are in time.

The farther away a reward is, the less emotionally real it feels.

A vacation next week feels exciting.

Retirement thirty years from now feels abstract.

A package arriving tomorrow feels tangible.

Financial freedom decades from now feels theoretical.

This is why knowing what to do and actually doing it are often two completely different things.

Most women understand that investing is important.

Most women understand that saving consistently matters.

Most women understand that compound growth can create extraordinary wealth over time.

The challenge isn't knowledge.

The challenge is that future rewards don't trigger the same emotional response as immediate ones.

Your brain sees the future, but it simply doesn't feel it.

The $10 Decision That Creates a $22,605 Difference

Let's look at a simple example.

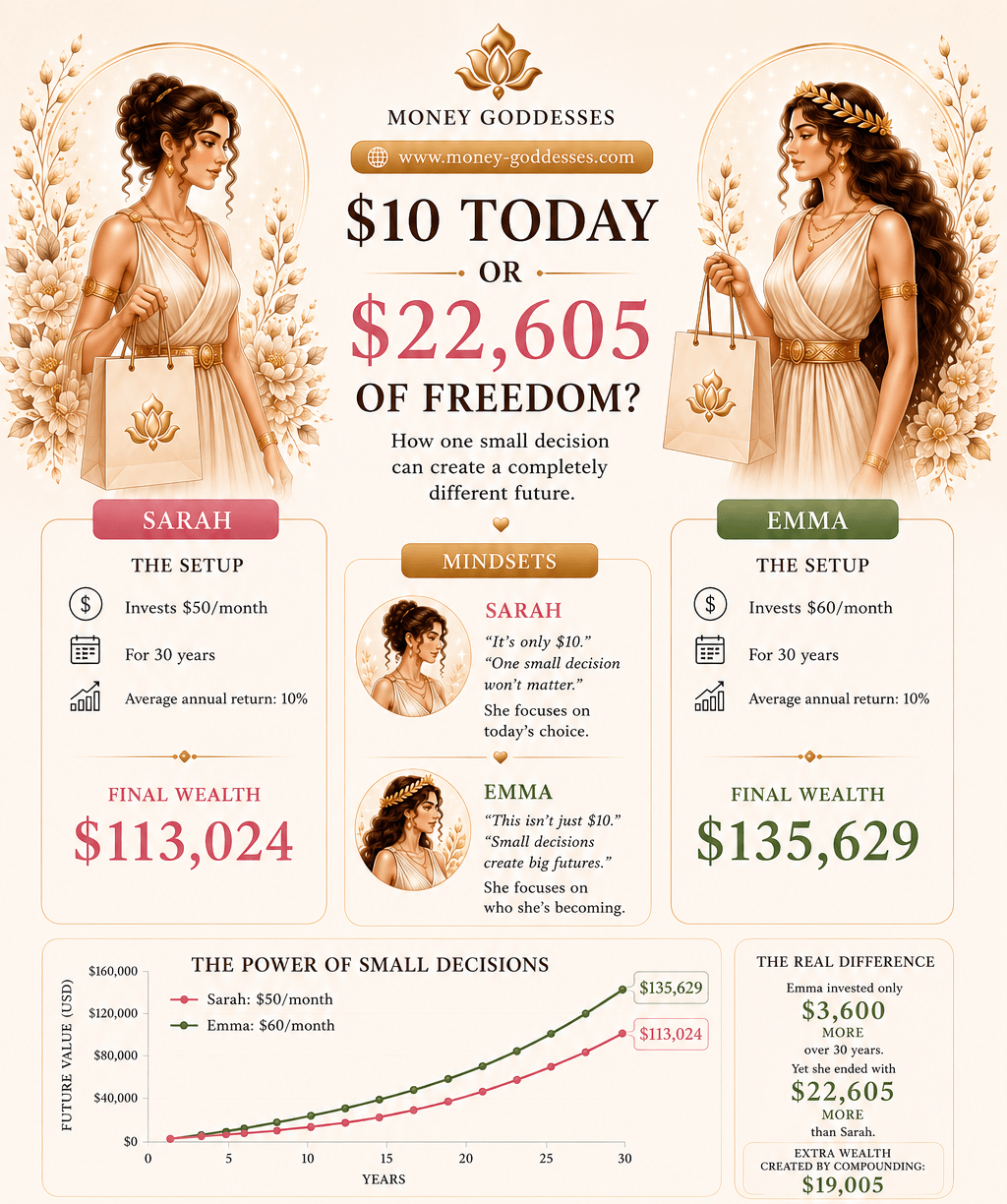

Sarah invests $50 per month for 30 years.

Emma invests $60 per month for 30 years.

Both earn an average annual return of 10%.

At the end of those 30 years, Sarah accumulates approximately $113,024.

Emma accumulates approximately $135,629.

The difference?

$22,605.

Now here's the fascinating part.

Emma only invested $10 more per month.

Over thirty years, that amounts to an additional contribution of just $3,600.

Yet that relatively small decision created $22,605 in additional wealth.

Even more remarkable, approximately $19,005 of that difference came from compound growth rather than Emma's own contributions.

The market created more wealth than Emma did -- that's the power of compounding.

And it's also a perfect example of why hyperbolic discounting can become so expensive.

When deciding whether to invest an extra $10 this month, your brain doesn't naturally compare $10 against $22,605.

It compares $10 against the immediate pleasure, convenience, comfort, or gratification that $10 can buy right now.

The future reward becomes psychologically discounted.

The present reward becomes psychologically amplified.

And that's where the trap begins.

The Lakshmi Shadow Behind Hyperbolic Discounting

If you've explored the Money Goddess archetypes, you'll recognize this dynamic immediately.

This is not Athena's shadow.

This is Lakshmi's shadow.

At her highest expression, Lakshmi teaches us to appreciate beauty, abundance, pleasure, luxury, and the richness of life.

She reminds us that money is meant to support a meaningful and joyful existence.

But in her shadow form, Lakshmi becomes attached to immediate gratification.

She prioritizes today's comfort over tomorrow's freedom.

She focuses on consumption instead of creation.

She seeks the reward now while discounting the value of future abundance.

The irony is that shadow Lakshmi often believes she is choosing abundance when she's actually sacrificing a much greater abundance later.

That extra coffee.

That impulse purchase.

That upgraded subscription.

That little luxury.

None of them seem significant on their own.

And that's exactly why they're so powerful.

The decision is never between a latte and financial freedom.

It's between a small present reward and a future reward your brain struggles to perceive.

The Surprising Science of Your Future Self

Researchers studying decision-making have discovered something fascinating.

When people think about themselves in the distant future, parts of the brain often respond similarly to how they respond when thinking about strangers.

In other words, your future self doesn't always feel like you.

She feels like someone else.

Someone you'll meet later.

Someone whose problems can wait.

Someone whose goals can be addressed tomorrow.

This helps explain why hyperbolic discounting is so persistent.

Every financial decision becomes a subtle competition between your present self and your future self.

Your present self wants comfort.

Your future self wants security.

Your present self wants convenience.

Your future self wants freedom.

And because your present self is sitting in the driver's seat, she usually wins.

Unless you change the game.

How Successful Investors Bypass Hyperbolic Discounting

The women who successfully build wealth don't necessarily have stronger willpower.

They don't wake up every month feeling excited to delay gratification.

They simply stop making the decision repeatedly.

They bypass hyperbolic discounting once.

Then they allow systems to take over.

This is why automation is one of the most powerful wealth-building tools available.

Instead of asking yourself every month whether you should invest another $10, you make the decision once.

You automate the transfer.

You automate the investment.

You remove the monthly debate between your present self and your future self.

The beauty of automation is that it doesn't require constant discipline.

It removes the opportunity for hyperbolic discounting to interfere.

Your future self no longer needs to compete for your attention every month because you've already chosen her.

The Real Cost of Small Decisions

One of the most important lessons in personal finance is that spending doesn't cost what you spend.

It costs what you could have owned instead.

Economists call this opportunity cost.

Most people think spending an extra $10 costs $10.

In reality, that $10 may cost thousands of dollars in future wealth.

The bill simply arrives decades later.

And because hyperbolic discounting makes future consequences feel less real, most people never connect today's choices with tomorrow's outcomes.

That's why so many women feel confused when they reach their 40s, 50s, or 60s and wonder where the years went.

The answer is rarely one catastrophic financial mistake.

It's usually thousands of tiny decisions that seemed insignificant at the time.

Make Hyperbolic Discounting Work for You

Here's the good news.

The same psychology that works against you can also work for you.

Once an investment becomes automatic, it quickly becomes normal.

You stop noticing the money leaving your account.

You adapt.

Your lifestyle adjusts.

And before long, your present self begins protecting the very habit she once resisted.

This is why the goal isn't to defeat hyperbolic discounting through willpower.

The goal is to design a system where it never gets a vote.

Discover Your Money Goddess

Do you tend to operate from Lakshmi's abundance -- or her shadow of immediate gratification?

Are other goddess archetypes quietly influencing your financial decisions without you realizing it?

Take the Unveil Your Inner Money Goddess Quiz and discover the hidden patterns shaping your relationship with money, investing, spending, and wealth.

Your future self is waiting to meet the woman you choose to become today.

Enjoy the Latest from the Blog

READY TO STEP INTO THE SANCTUARY OF ABUNDANCE?

Join real women building confidence, clarity, and wealth for $9/month.