Why Women Start Investing Too Late: The Hidden Cost of Waiting

"I just want to learn a little more first."

It's one of the most common things I hear from women when we begin talking about investing.

Not because they're irresponsible with money.

Not because they don't care about their future.

In fact, it's often the opposite.

The women who delay investing are frequently the most thoughtful, intelligent, and conscientious women I meet. They want to understand what they're doing before they commit their hard-earned money. They want to avoid mistakes. They want to feel confident.

And yet, this desire to be fully prepared before taking action can quietly become one of the biggest obstacles to building wealth.

If you've taken my Money Goddess quiz, you may recognize this as one of Athena's shadow patterns.

Athena, the Goddess of Wisdom, strategy, and knowledge, is a powerful ally when it comes to managing money. She encourages us to learn, plan, research, and make informed decisions. But when her energy becomes imbalanced, wisdom turns into overthinking, preparation becomes procrastination, and learning becomes a substitute for action.

Instead of taking the first step, we convince ourselves that we need one more book, one more podcast, one more course, one more certification, one more raise, or one more year of financial stability before we're truly ready to invest.

Meanwhile, something incredibly important is happening in the background.

Time keeps moving.

And when it comes to investing, time is often far more valuable than knowledge.

Why Time Is the Most Powerful Wealth-Building Tool for Women to Start Investing

Many people assume that building wealth is primarily about how much money you invest.

While the amount certainly matters, there is another factor that is often far more powerful: the length of time your money has to grow.

This is the principle behind compounding — the process through which your investments generate returns, and those returns begin generating returns of their own.

Albert Einstein allegedly called compound interest the eighth wonder of the world. Whether he actually said it or not, the principle itself remains extraordinary.

Compounding creates a snowball effect. In the beginning, progress appears slow. The numbers feel small. It may even seem as though nothing significant is happening.

But as the years pass, growth begins accelerating. The returns generated in earlier years start producing their own returns, and eventually the snowball becomes impossible to ignore.

The challenge is that compounding rewards patience, not urgency.

Its greatest benefits appear decades later.

Which means every year you delay investing is a year that compounding never gets the opportunity to work for you.

Two Women Start Investing: The Tale of Sarah and Emma

Let's look at a simple example.

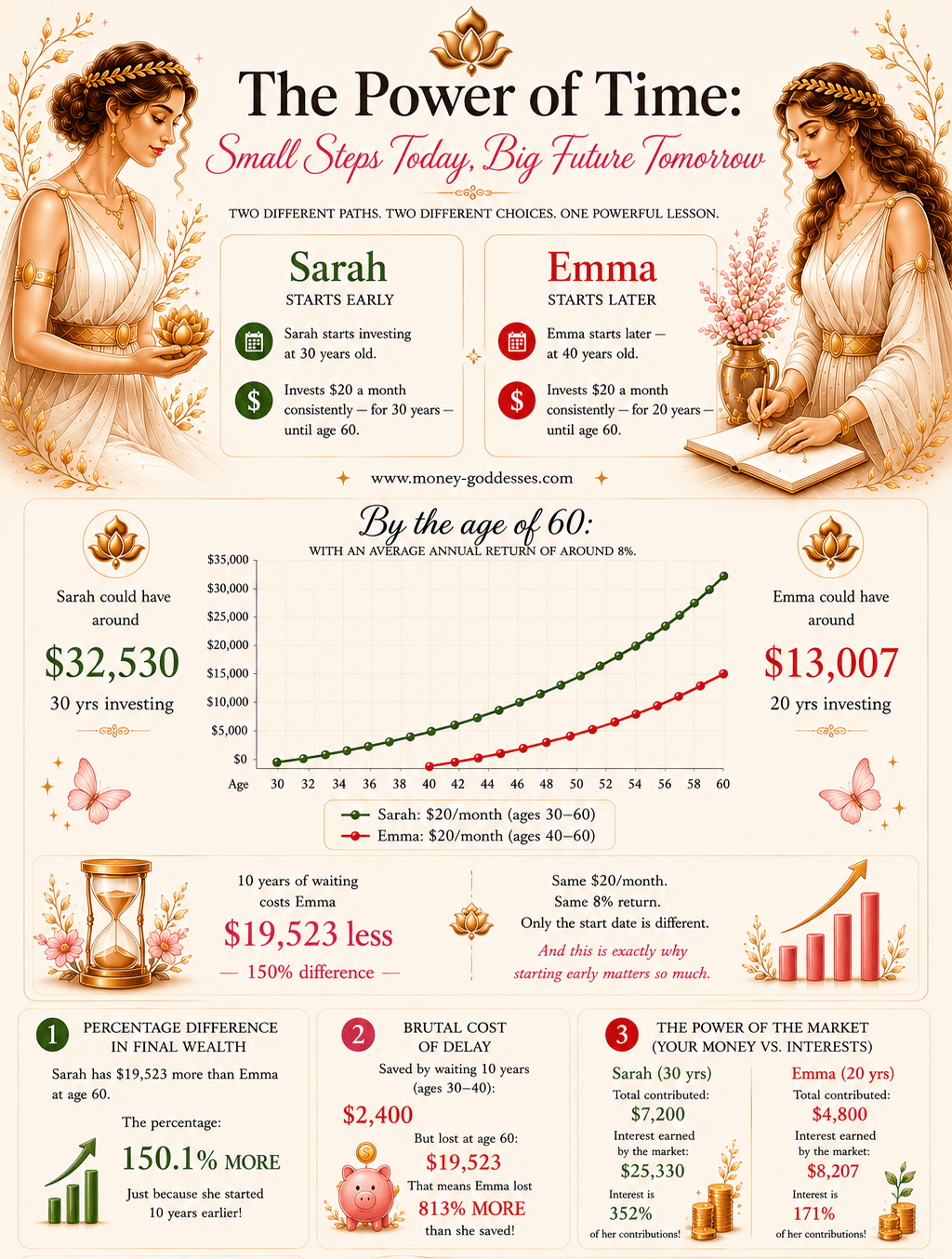

Sarah begins investing at age 30.

Emma begins investing at age 40.

Neither woman is wealthy. Neither woman has access to insider information. Neither woman chooses a magical investment that outperforms the market.

In fact, they do exactly the same thing.

Both invest just $20 per month.

Both earn an average annual return of 8%.

The only difference is that Sarah gives her money ten additional years to grow.

By age 60, Sarah has contributed a total of $7,200.

Emma has contributed $4,800.

At first glance, that doesn't seem like a dramatic difference. Sarah only invested $2,400 more than Emma over the course of their lives.

Yet by age 60, Sarah's account has grown to approximately $32,530, while Emma's account has reached only $13,007.

That ten-year delay costs Emma $19,523.

Sarah ends up with approximately 150% more wealth — not because she was smarter, luckier, or more financially sophisticated, but because she started earlier.

This is the true power of time.

The Number That Surprised Me Most

What I find most fascinating isn't the final account balances. It's what happened beneath the surface.

Emma saved $2,400 by waiting ten years before she started investing.

Many people would view that as a reasonable trade-off.

After all, she kept that money available for other priorities.

But by age 60, the cost of waiting wasn't $2,400.

It was $19,523.

In other words, Emma lost 813% more than she saved.

Read that again.

She avoided investing $2,400 and ultimately gave up nearly twenty thousand dollars of future wealth.

This is why waiting is so dangerous.

The cost isn't visible.

You never receive a bill for the growth you didn't earn.

There is no notification telling you what your money could have become.

The opportunity simply disappears quietly, year after year.

What the Market Earned Was Greater Than What They Invested

Another powerful lesson emerges when we look at where Sarah and Emma's wealth actually came from.

Sarah contributed $7,200 over thirty years.

Yet by age 60, approximately $25,330 of her final balance came from investment growth rather than her own contributions.

That means the market generated roughly 352% of what she personally invested.

Emma's investments also grew, but she earned approximately $8,207 in market gains on her $4,800 contribution.

That's about 171% of what she invested.

Still impressive. But nowhere near what Sarah achieved.

The lesson is profound.

Sarah didn't build wealth primarily through saving. She built wealth by giving her investments time to multiply.

The market did most of the heavy lifting.

Why Women Start Investing Later Than They Need To

For many women, the obstacle isn't a lack of money. It's a lack of confidence.

We want certainty before taking action. We want guarantees before taking risks. We want to feel fully prepared before stepping into unfamiliar territory.

Yet investing rarely rewards perfection.

It rewards participation.

The women who build wealth aren't necessarily the women who know the most. They're often the women who begin before they feel completely ready.

They open the account.

They invest the first $20.

They automate the contribution.

They allow consistency and time to do their work.

Knowledge matters. Financial education matters. But eventually Athena must step out of her shadow.

There comes a moment when learning must become doing.

Your Future Wealth Is Being Created Today

Every investment decision contains two ingredients: money and time.

Most people spend their lives focusing on the first one. Successful investors learn to respect the second.

Because money can always be earned again.

Time cannot.

The good news is that you don't need thousands of dollars to begin.

You don't need perfect market conditions. You don't need to become an expert first.

You simply need to start.

The smallest investment made today has more power than the perfect investment postponed indefinitely.

Discover Your Money Goddess

If you've been waiting to invest because you're still trying to feel ready, perhaps it's time to explore which goddess archetype is influencing your relationship with money.

Are you operating from Athena's wisdom — or her shadow?

Are other goddess energies shaping your financial decisions without you realizing it?

Take the Unveil Your Inner Money Goddess Quiz and discover the hidden money patterns, strengths, and blind spots influencing your financial journey.

Your future self is being shaped by the choices you make today.

Enjoy the Latest from the Blog

READY TO STEP INTO THE SANCTUARY OF ABUNDANCE?

Join real women building confidence, clarity, and wealth for $9/month.